#1

La SEC complicará seguir las carteras de los hedge funds

Para varios de los que estamos encantados con el servicio de Dataroma o Whalewisdom que nos permiten ver los movimientos de los principales hedge funds norteamericanos de forma gratuita, se nos puede complicar acceder a esta información.

Os adjunto el comunicado, sobre la nueva propuesta de la SEC de dispensar por tamaño la publicación de los movimientos de estos vehículos.

Os adjunto el comunicado, sobre la nueva propuesta de la SEC de dispensar por tamaño la publicación de los movimientos de estos vehículos.

SEC Proposes Amendments to Update Form 13F for Institutional Investment Managers; Amend Reporting Threshold to Reflect Today’s Equities Markets

FOR IMMEDIATE RELEASE

2020-152

2020-152

Washington D.C., July 10, 2020 —

The Securities and Exchange Commission today announced that it has proposed to amend Form 13F to update the reporting threshold for institutional investment managers and make other targeted changes. The threshold has not been adjusted since the Commission adopted Form 13F over 40 years ago.

Form 13F was adopted pursuant to a 1975 statutory directive designed to provide the Commission with data from larger managers about their investment activities and holdings, so that their influence and impact could be considered in maintaining fair and orderly securities markets.

“Monitoring equity holdings of large institutional investment managers is an important part of our regulation and oversight of the securities markets,” said SEC Chairman Jay Clayton. “Today’s proposal will update, for the first time in over 40 years, the 13F reporting threshold to a level that furthers the statutory goal of enabling the SEC to monitor holdings of larger investment managers while reducing unnecessary burdens on smaller managers.”

New Reporting Threshold

In 1978, when Form 13F was adopted, the threshold for filing the form was set at $100 million, the amount in the underlying statute and representing a certain proportionate market value of U.S. equities. Since then, the overall value of U.S. public corporate equities has grown over 30 times (from $1.1 trillion to $35.6 trillion), and the relative significance of managing $100 million has declined considerably. The Commission and staff have received recommendations to revisit the Form 13F reporting threshold from a variety of sources over the years, including from the Commission’s Office of the Inspector General.

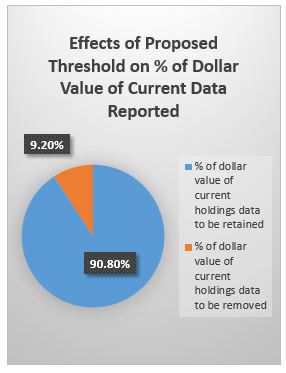

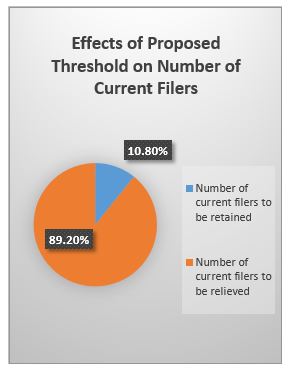

Today’s proposal would raise the reporting threshold to $3.5 billion, reflecting proportionally the same market value of U.S. equities that $100 million represented in 1975, the time of the statutory directive. The new threshold would retain disclosure of over 90% of the dollar value of the holdings data currently reported while eliminating the Form 13F filing requirement and its attendant costs for the nearly 90% of filers that are smaller managers. In addition, since the initial 13F thresholds were established in 1978, the Commission has added other data collection tools, including N-PORT.

The proposal includes an analysis of alternate approaches to adjusting the reporting threshold, including the use of consumer price inflation and stock market returns; the increase in Form 13F filers over the past four decades; and the increase in the overall size of the U.S. equities market over time. Under the proposed amendments, the aggregate value of section 13(f) securities reported by managers would represent approximately 75% of the U.S. equities market as a whole, as compared with 40% in 1981, the earliest year for which Form 13F data is available.

Relief for Smaller Managers

The legislative history of the 1975 statute indicates that the reporting threshold of $100 million was intended to capture the largest institutional managers. The proposed adjusted threshold would provide relief to smaller managers who are now subject to Form 13F reporting, while retaining data on over 90% of the dollar value of the securities currently reported.

The proposal includes an analysis of the estimated costs and burdens on smaller managers in filing Form 13F. For example, the proposal estimates that total annual direct compliance cost savings for smaller managers who would no longer file reports on Form 13F would range from $68.1 million to $136 million. In addition, the proposal discusses indirect costs faced by smaller managers, such as those associated with potential front-running and copycatting, which may increase the costs of investing for smaller managers and hinder their investment performance, with potential effects on their portfolios’ owners.

Other Proposed Changes

Recognizing that market conditions will continue to evolve, the proposal also would direct the staff to review the Form 13F reporting threshold every five years and recommend an appropriate adjustment, if any, to the Commission. Additionally, the proposal would eliminate the ability of managers to omit certain small positions, thereby increasing the overall holdings information required from larger managers. The proposal also would require managers to report additional numerical identifiers to enhance the usability of the information provided on the form, and amend the instructions relating to requests for confidential treatment of Form 13F information.

Request for Comment

The proposal will be published on the Commission’s website and in the Federal Register. There will be a 60-day comment period following publication in the Federal Register.

The proposal includes specific requests for comment on the proposed threshold, and whether an alternative method to adjust the threshold should be considered, as well as on the estimates of the burdens and costs to investment managers, particularly smaller managers, in preparing and filing Form 13F.

* * *

FACT SHEET

Reporting Threshold for Institutional Investment Managers

Action

The Commission is proposing to raise the reporting threshold for Form 13F and to make certain other changes to the form.

Background

Section 13(f) of the Securities and Exchange Act was adopted as part of the Securities Acts Amendments of 1975 (“1975 Amendments”). Section 13(f) requires a manager to file a report with the Commission if the manager exercises investment discretion with respect to accounts holding certain equity securities (“13(f) securities”) having an aggregate fair market value on the last trading day of any month of any calendar year of at least $100 million. Section 13(f) also gives the Commission broad rulemaking authority to determine, among other things, the size of the institutions required to file reports and the authority to raise or lower the threshold.

In 1978, the Commission adopted Rule 13f-1, requiring managers to file quarterly reports on Form 13F if the accounts over which they exercise investment discretion hold an aggregate of more than $100 million in 13(f) securities.

Highlights

The proposed amendments to Form 13F and rule 13f-1 under the Securities Exchange Act of 1934 would raise the threshold for reporting specified equity securities on Form 13F from $100 million to $3.5 billion, the first change to the threshold since the form was adopted in 1978. The proposal would also direct the staff to conduct reviews of the Form 13F reporting threshold every five years and recommend an appropriate adjustment to the Commission, if the staff believes after such review that additional adjustments should be made to the threshold.

The proposed adjusted threshold is based on the growth of the U.S. equities market that occurred between the adoption of section 13(f) in 1975 and December 2018, and is intended to reflect proportionally the same market value of U.S. equities that $100 million represented in 1975. The adjusted threshold is designed to achieve the goals of Form 13F–including the submission of filings by larger managers that cover a large proportion of managed assets, while limiting the burdens of reporting and minimizing the number of filers–as applied to today’s market size. In 1975, filers representing holdings of approximately 75% of the dollar value of all institutional equity security holdings were subject to the reporting requirements. Under the increased threshold, similarly, the aggregate value of securities reported by managers would represent approximately 75% of the U.S. equities market as a whole. As shown in the following charts, the proposal would retain disclosure of over 90% of the dollar value of holdings data currently disclosed through Form 13F, while exempting smaller asset managers, who represent the majority of current filers.

* Source: The estimates in these figures are based on SEC staff analysis of Form 13F holdings data reported by institutional investment managers as of December 31, 2018.

In addition, the proposal would eliminate the omission threshold that currently permits managers to exclude from the form certain small positions. The proposal also would (a) require managers to report certain numerical identifiers to enhance the usability of the information provided on Form 13F; (b) make certain technical amendments to modernize the information reported on Form 13F; and (c) conform the standard for SEC review of requests for confidential treatment of Form 13F information with a recent decision by the U.S. Supreme Court.

Possible Reduction in Costs and Burdens to Smaller Managers

The proposal describes and requests comment on direct compliance costs associated with Form 13F, including (1) developing and maintaining internal hardware and software systems, (2) utilizing internal and external legal and compliance resources for advice and review, including analysis of whether holdings qualify for confidential treatment, (3) preparing the information for submission, and (4) undertaking other reviews or compliance activities as part of the manager’s overall compliance program. The proposal estimates that, for smaller managers that would no longer file reports on Form 13F under the proposed threshold, these direct compliance costs could range from $15,000 to $30,000 annually per manager, depending on certain factors, resulting in direct compliance cost savings for these managers per year ranging from $68.1 million to $136 million.

The proposal also describes and requests comment on indirect costs associated with Form 13F, including the use of Form 13F data by other market participants to engage in front running (which primarily harms the owners of a portfolio) or copycatting (which potentially harms the portfolio manager) of the investment portfolios of smaller managers, which may increase the costs of investing for smaller managers and hinder their investment performance, with potential effects on their portfolios’ owners. In addition, the proposal discusses (a) the costs to smaller managers of requesting confidential treatment of Form 13F information and (b) costs to the Commission associated with staff time and resources spent addressing smaller managers’ inquiries and requests for assistance regarding compliance with Form 13F reporting obligations.

The proposal includes adjustments to the existing burdens for Form 13F for purposes of the Paperwork Reduction Act of 1995, and requests comment on those adjustments, as well as the initial and ongoing annual burden estimates associated with the proposed amendments to Form 13F.